Control what you can control

- Brett Watt

- Aug 27, 2019

- 4 min read

Updated: Dec 6, 2019

The growth of passive investing over the course of the last 10 years has been astounding… and let’s be honest it is a great thing! In 2018, passive index funds grew to 37% market share in the U.S., reaching about $453 billion, while actively managed mutual funds saw a $304 billion outflow according to research done by Bloomberg. In Canada we are observing growth in passive investments but at a much slower pace than our counterparts in the U.S., as passive funds have a market share of about 10% in 2018.

Let’s review why many are making the transition from the old school active approach to passive investing. Each year there is a scorecard published on Active vs Passive investing and how each has performed. By the end of 2018, approximately 92% of active large-cap core stock fund managers over the past 15 years had under-performed the S&P 500 net of fees. In addition, this was the ninth year in a row that a majority of actively managed funds in the U.S., have lost to the index. That is scary, right? Not only is the average active manager under-performing but are also charging higher fees.

As advisers, we could attend numerous conferences, listen to fund managers speak and meet with representatives from the actively managed fund marketplace. Through my time as an adviser, a common theme in these conversations is that we have been on one of the largest bull market runs in the history of the stock market. This is going to end, of course, we agree on this. One thing I often questioned is where the active fund managers are providing value. To this, we found a common trend, which was that active fund managers can really add value to a client’s portfolio when the stock market is experiencing volatility and in times where the markets are down. In 2018, a time of heightened volatility and negative annual returns, the data shows this tale did not prove to be the case!

To note- for the sake of keeping this article a reasonable length. We have attached data from the U.S only. In the footnote you will find a link to the SPIVA scorecard which shows data for international equity and fixed income. The under-performance trend continues in each of theses asset classes as well.

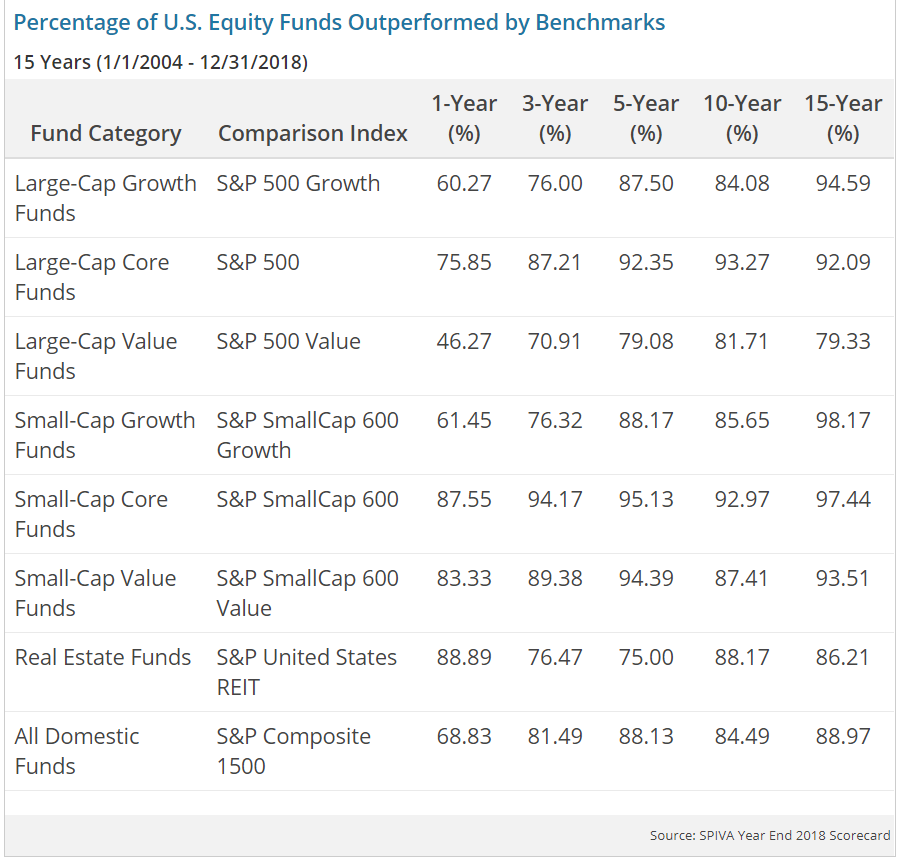

The table below shows the percentage of a selection of active domestic equity funds that under-performed their respective benchmarks over one-, three-, five-, 10- and 15-year periods ending Dec. 31, 2018.

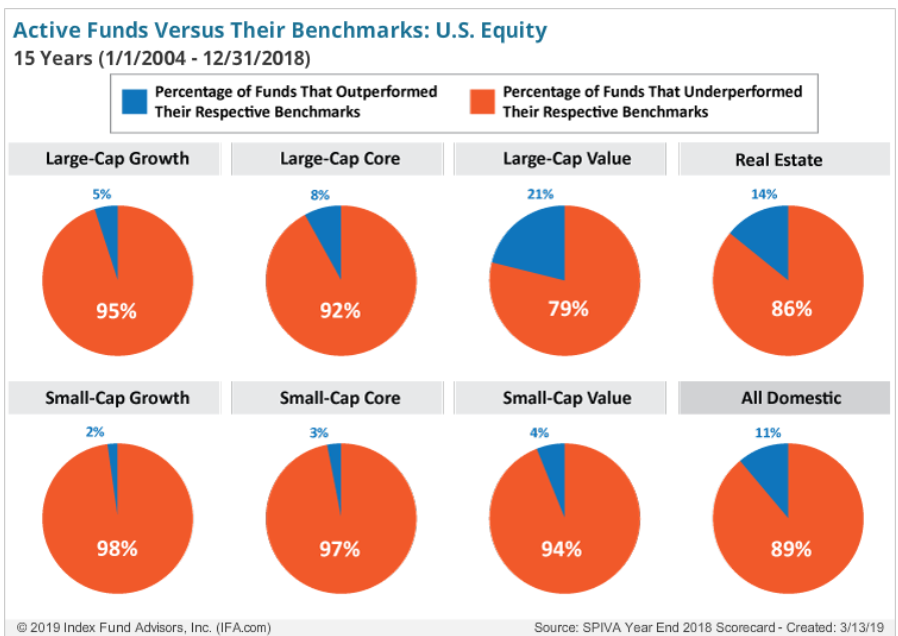

The pie charts below show the percentage of active U.S. equity funds that under-performed their respective benchmarks for the 15-year period ending Dec. 31, 2018.

The SPIVA report card is a great resource for those objectively trying to track how active fund managers have performed against their indexes. Unfortunately, picking these 1 in 20 outperforming managers in advance has proven to be impossible.

When looking at the data one will see that there is out-performance, but does this help us at all? The common theme is that the out-performance is more prevalent in the early years. The problem for an investor and an active manager is having the consistency to outperform the respected benchmarks. So, with that the question becomes is the out performance luck or skill? Our belief is we that we cannot rely on an active manager and the data from 2018 is yet another sobering check for an active manager’s empty promises. An investor should focus on what they can control vs trying to gamble on something the chances of winning are very low. Let’s view the markets as an ally, not an adversary.

This publication contains opinions of the writer and may not reflect opinions of Manulife Securities Investment Services Inc. The information contained herein was obtained from sources believed to be reliable, but no representation, or warranty, express or implied, is made by the writer or Manulife Securities Investment Services Inc. or any other person as to its accuracy, completeness or correctness. This publication is not an offer to sell or a solicitation of an offer to buy any of the securities. The securities discussed in this publication may not be eligible for sale in some jurisdictions. If you are not a Canadian resident, this report should not have been delivered to you. This publication is not meant to provide legal or account advice. As each situation is different you should consult your own professional Advisors for advice based on your specific circumstances

"Manulife Securities Investment Services Inc. does not make any representation that

the information provided in the 3rd Party articles is accurate and will not accept any

responsibility or liability for any inaccuracies in the information or content of any 3rd party

articles.

Any opinion or advice expressed in the 3rd party article, including the opinion of a Manulife

Securities Advisor, should not be construed as, and may not reflect, the opinion or advice of

Manulife Securities. The 3rd party articles are provided for information purposes only and

are not meant to provide legal accounting or account advice.”

Comments